Europe Access to Energy Research Brief

Download the research brief here

Introduction

Europe is a highly developed region and Europeans rarely have difficulty accessing the electricity or gas grid. However, price volatility means that poorer Europeans are often at risk of being cut off from either electricity or heatingAviles, Luis Anibal. “Electric Energy Access In European Law: A Human Right?” Columbia Journal of European Law 19 (2012). http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2008887.. In fact, access to energy challenges in Europe are two-fold. First, cost: European countries have some of the highest energy prices among OECD countries. By 2030, it is estimated that energy costs in the European Union (EU) will be 50 per cent higher than energy prices in the United States, and three times higher than prices in ChinaBuzek, Jerzy. “Europe’s Malfunctioning Energy Market Is Stifling Economic Growth.” EnergyPost, August 8, 2013. http://www.energypost.eu/europes-malfunctioning-energy-market-is-stifling-economic-growth/.. These high prices not only restrict access by placing a disproportionate burden on the poorest members of society, they also constrain economic growth by increasing the costs of all goods and services. The second major access to energy challenge facing Europe is energy security, or more specifically, the geo-political negotiations that ensure a stable flow of energy into the region for the foreseeable future. Currently, Europe imports 53 per cent of all energy it uses, at a cost of more than one billion euros (US$1.14 billion) each dayThe European Commission. “Imports and Secure Supplies.” Energy, October 26, 2015. http://ec.europa.eu/energy/en/topics/imports-and-secure-supplies.. Therefore, the infrastructure and political investments to ensure energy security are vital in stabilizing regional energy prices, and thus access to energy. Both of these challenges are interrelated, as the consequence of poor energy security and over-reliance on exports is often high prices.

The Single Internal Energy Market

The European Commission has undertaken a major effort to streamline the European energy market, increase competition and consumer option, and lower prices by developing a single internal energy market for electricity and gas. The development of a single European market requires building major infrastructure connections between countries. For example, electricity grids in the Iberian Peninsula, the Baltic region, and the United Kingdom are not linked to each otherThe European Commission. “Single Market Progress Report.” Energy, 2014. https://ec.europa.eu/energy/en/topics/markets-and-consumers/single-market-progress-report.. Gas infrastructure is also poorly connected across the continent. The Baltic states are not connected to the main European gas grid, and instead receive the majority of their gas supplies from a single liquefied natural gas (LNG) port in Lithuania, with Russian imports making up the remainderPolak, Petr. “Europe’s Low Energy.” Foreign Affairs, September 9, 2015. https://www.foreignaffairs.com/articles/western-europe/2015-09-09/europes-low-energy.. The result of all this disjointed energy infrastructure is that prices vary widely across the continent. Wholesale gas prices in Tallinn, Estonia can be 50 per cent more expensive than in London and electricity can be almost 70 per cent more expensive in Rome than in TallinnBuzek, 2013..

When it comes to gas, Western and Eastern Europe tell very different stories. Western Europe’s natural gas market is highly developed, with LNG terminals, large storage facilities, and reverse flow pipeline options. All of this infrastructure makes Western Europe attractive to diverse global suppliers, giving the region a natural resilience to global price fluctuationsBoersma, Tim. “Europe’s Energy Dilemma.” The Brookings Institution, June 18, 2014. http://www.brookings.edu/research/articles/2014/06/18-europes-energy-dilemma-boersma.. Eastern Europe, in contrast, is heavily reliant on Russian gas imports, a fact explained by both geography and political history. Natural gas is not available in the eastern part of the continent, and so eastern countries have historically built their economies on readily available coal, and to a lesser extent, oil. With the EU’s current concerns about climate change and greenhouse gas (GHG) emissions, Eastern countries have had to transition away from coal. The only realistic short-term substitute to meet the region’s energy needs is natural gas. However, because gas has historically contributed only modestly to the energy portfolio in Eastern Europe, infrastructure is not well connected and regulatory frameworks are outdated. Therefore, the region relies almost exclusively on Russian imports, making arbitrary pricing the norm rather than the exception Boersma, 2014.. After a three-year investigation, the European commission concluded that Russia’s gas-exporting monopoly Gazprom had abused its position as sole supplier to a number of Eastern European countries by charging inflated rates and prohibiting those countries from re-selling gas to other European countriesPolak, 2015..

A more integrated market would theoretically lower overall energy prices at the consumer level by increasing competition among producers and smoothing out the possibility of sharp price fluctuations. Many of the projects that are essential for regional connection, however, are not commercially viable, and therefore the market is expected to only provide half the necessary investmentThe European Commission. “Infrastructure.” Energy, 2015. https://ec.europa.eu/energy/en/topics/infrastructure.. Although it is clear that the remaining half must be met by governments, the EU is facing serious obstacles in achieving regional cooperation. For example, politicians from all EU member states have been eager to ensure that a portion of the 5.85 billion euros (US$6.65 billion) available under the Connecting Europe Facility (which is still only a tiny portion of the estimated 200 billion euros (US$227.5 billion) necessary for full integration The European Commission. “Infrastructure.” 2015.) be spent in their home countries. This wide dispersal of financial means makes money available for feasibility studies, but not much else. Under the current system, price shocks still threaten the resilience of Eastern and Southern EuropeBoersma, 2014..

Progress Toward Renewable Energy

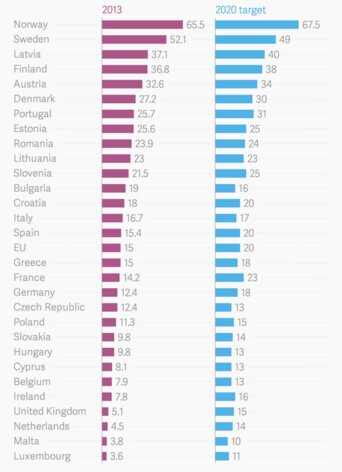

One method that Europe could use to increase energy security is a greater reliance on renewable resources. In fact, this is a major goal of the EU, and goes hand in hand with the development of a single regional energy market. Greater connectivity increases the viability of renewable resources because, when the wind is not blowing in Germany, it is likely sunny in Spain, and when it is cloudy in Spain, there is a river flowing through a turbine in France. To achieve renewable energy goals, in 2008 the EU set a binding target of 20 per cent of final energy consumption from renewables by 2020The European Commission. “Renewable Energy.” Energy, 2015. https://ec.europa.eu/energy/en/topics/renewable-energy.. To achieve this target, each country then set their own national renewable energy goals based on progress at the time, available resources, and relative wealthEvans, Simon. “Five Charts Showing the EU’s Surprising Progress on Renewable Energy.” Carbon Brief, March 11, 2015. http://www.carbonbrief.org/five-charts-showing-the-eus-surprising-progress-on-renewable-energy/.. The most recent reports show that three European countries — Sweden, Bulgaria and Estonia — have already surpassed their own goals, with the EU as a whole currently at 15 per cent. Figure 1 shows each European country’s 2013 share of renewable energy next to their 2020 national goal.

Support Scheme Policies

Progress toward these goals is made on two fronts: rationally designed support schemes for renewables that avoid disrupting the larger energy market, and falling overall energy use The European Commission. “Renewable Energy.” 2015.. One particularly successful support scheme is the feed-in tariffs (FITs) that have been used to encourage solar panel installation in Germany. Feed-in tariffs work by basically guaranteeing an electricity price for a set timeframe (usually about 20 years) for producers of solar photovoltaic (PV) energy. That power is purchased by utility companies at the guaranteed rate, and then distributed to the wider grid. The utility companies are then reimbursed by the government, which collects a “renewables levy from most electricity consumers.” This support scheme eliminates the risk of investing in solar PV, as producers are able to calculate exactly how much they will make over the lifespan of their purchased PV arrayWeiss, 2014.. The FIT system has been so successful that in 2013 Germany reached 35 gigawatts of solar PV capacity, with about seven GW being added each yearWeiss, Jurgen. “Solar Energy Support in Germany: A Closer Look.” The Brattle Group, July 2014. http://www.seia.org/sites/default/files/resources/1053germany-closer-look.pdf. (compared to the United States’ total installed solar PV capacity of 22.7 GW in 2015SEIA. "U.S. Solar Market Insight." Solar Energy Industries Association, September 9, 2015. http://www.seia.org/research-resources/us-solar-market-insight). Germany has also been credited with dramatically driving down the cost of solar PV, as demand stimulated by the FIT surges. In fact, the FIT system has been so successful that Germany has had to repeatedly adjust downwards the guaranteed rate for electricity produced with solar PVWeiss, 2014.. The major complaint from critics of Germany’s FIT program is that it has driven up costs for consumers, in effect limiting access to energy for poorer German citizens. However, while it is true that Germany’s renewables levy (about six euro cents per kilowatt-hour; US$0.07/KWh) is significant in increasing electricity prices (about 30 euro cents per KWh; US$0.34/KWh), other taxes and fees also contribute a similar amount to prices, meaning that even without FITs, Germany would still have some of the highest electricity prices in the worldIbid.. Therefore, German policies can provide a positive blueprint for other countries seeking to increase their energy security by relying more heavily on renewable resources.

Energy Efficiency

The cheapest and most efficient way to ensure that everyone has affordable access to energy is of course for each person to use lessECEEE. "European Competitiveness and Energy Efficiency: Focusing on the Real Issue." European Council for an Energy Efficient Economy, May 21, 2013. http://www.eceee.org/policy-areas/competitiveness/ee-and-competitiveness.. This is exactly what is occurring across Europe; today, the EU uses as much energy as it did in 1990, although some of this decrease may be due to the slump in demand following the 2008 financial crisisEvans, 2015.. Interestingly, the high energy prices across Europe that are often cited as a challenge to be overcome are also largely instrumental in encouraging energy efficiency in industry and residential appliancesZachmann, Georg. “What Should Europe Do about High Energy Prices?” Bruegel, March 12, 2014. http://bruegel.org/2014/03/what-should-europe-do-about-high-energy-prices/The European Commission. “Energy Efficiency.” Energy, 2015. https://ec.europa.eu/energy/en/topics/energy-efficiency.. Many reports on energy in Europe also identify energy efficiency as a key strategy for European industry and other businesses to remain competitive with the United States, where energy is significantly cheaper. Following the 2008 financial crisis and ensuing recession, global oil prices have slumped dramatically. The result will likely be lower external gas bills for European nations — a welcome respite for the continent. Lower prices will not continue forever, however, and to remain globally competitive, European nations need to use this freed-up investment capacity to fund energy efficiency initiatives that will move the EU toward its goal of 20 per cent greater efficiency by 2020EEFIG, 2015..